The Real Estate Council of Ontario has issued a discipline decision regarding a broker who failed to inform his international clients about significant tax obligations associated with their purchase of a residential property. Marius Kerkhoff, a registered broker at the time with RE/MAX A-B Realty Ltd., faced a disciplinary proceeding following a real estate transaction in Norwich, Ontario. The case centered on the application of the Non-Resident Speculation Tax, a provincial levy that applies to foreign nationals purchasing residential real estate in certain parts of Ontario. The decision, released on January 16, 2026, details a series of professional failures that resulted in a substantial financial burden for the buyers and subsequent penalties for the broker involved.

The transaction involved Leendert Marinus Geluk and Adriana Chilia Geluk-Romijn, who were identified as the buyers of a residential property in the Norwich area. At all relevant times during the purchase process, the buyers were foreign nationals and did not hold permanent residency status in Ontario or any other Canadian province. Because of their residency status, their purchase was subject to the Non-Resident Speculation Tax. This tax is a one-time payment required from foreign individuals or entities who are not Canadian citizens or permanent residents when they acquire residential property. By October 2022, the provincial government had set this tax rate at 25 percent of the total purchase price for applicable properties in Ontario.

Marius Kerkhoff acted as the representative for the buyers through his brokerage. According to the agreed statement of facts submitted during the discipline proceedings, Kerkhoff was aware of the existence of the Non-Resident Speculation Tax in a general sense. However, the broker operated under the mistaken belief that the tax was no longer in effect after January 2024. Despite knowing that his clients were international buyers, he did not inform them that this tax might apply to their acquisition of the Norwich property. This lack of communication regarding a significant financial obligation formed the basis of the regulatory investigation into his conduct as a registered real estate professional.

The sequence of events revealed that the buyers were left unaware of the potential 25 percent surcharge throughout the initial phases of the transaction. The agreed statement of facts indicates that Kerkhoff did not advise his clients to seek independent legal advice before they submitted an offer on the property. This step is a standard practice in real estate transactions, particularly when complex legal or tax implications such as foreign buyer levies are involved. By failing to recommend legal counsel, the broker missed an opportunity for the buyers to be properly briefed on the financial realities of the purchase by a qualified legal professional.

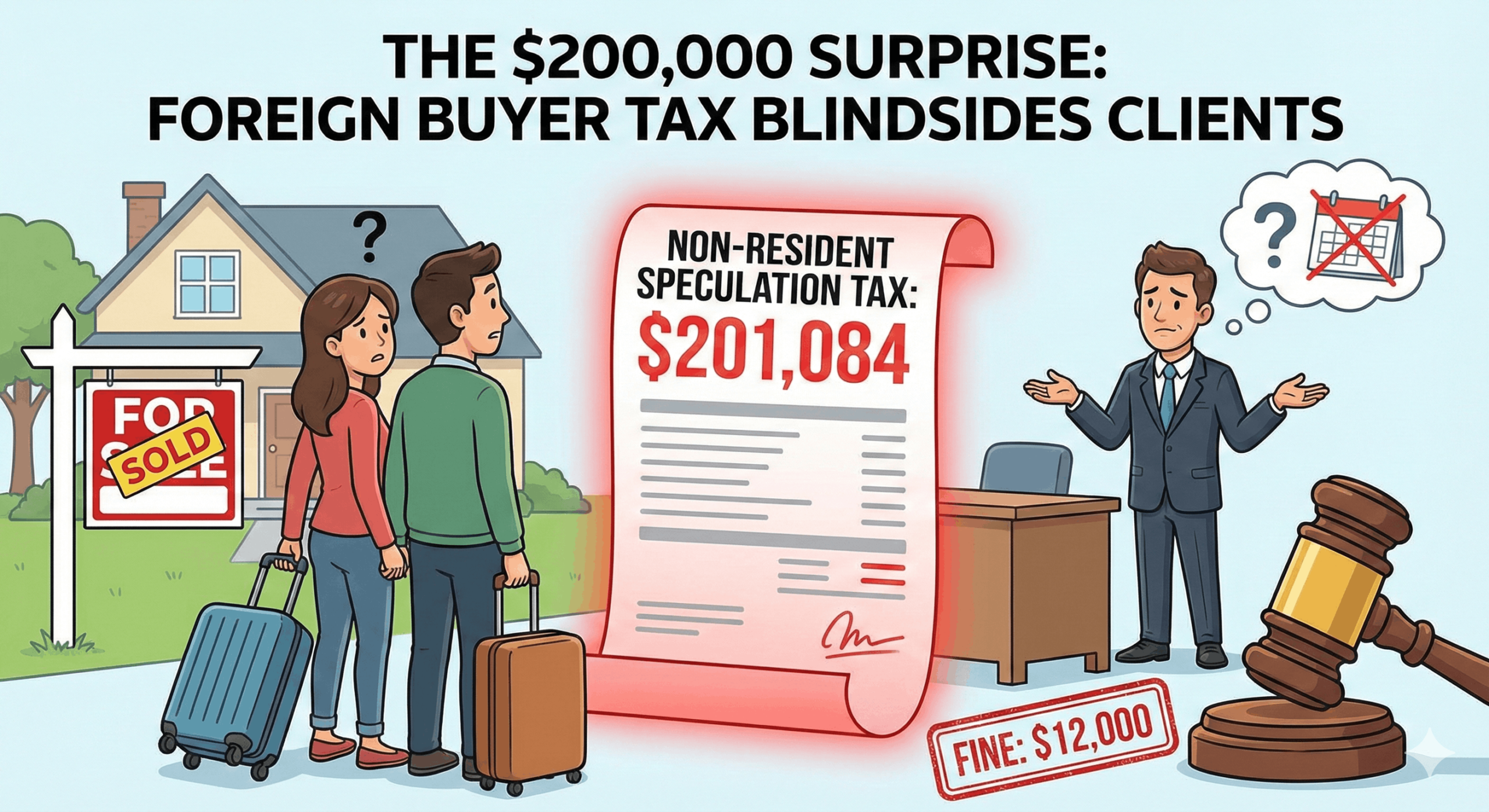

The oversight remained undiscovered until very late in the closing process. The buyers only became aware of their obligation to pay the Non-Resident Speculation Tax approximately one week before the scheduled completion date of the Agreement of Purchase and Sale. Remarkably, the information did not come from their own representative, but rather from the vendor of the property. Upon learning of the requirement, the buyers were faced with a significant financial shortfall. The total amount required to satisfy the tax obligation was $201,084.07. This was a sum the buyers had not factored into their budget, as it was in addition to the total amount they had expected to pay for the property based on the information provided during the representation.

The disciplinary committee noted that the buyers would have taken this tax into consideration before entering into a binding Agreement of Purchase and Sale if it had been brought to their attention by their broker. The failure to disclose this material fact meant that the clients were making one of the largest financial decisions of their lives without a complete understanding of the total cost. The subsequent investigation by the Real Estate Council of Ontario determined that Kerkhoff’s actions and omissions constituted several violations of the Trust in Real Estate Services Act, which is the legislation governing the conduct of real estate professionals in the province.

The findings of the discipline committee specifically cited violations of both the Code of Ethics and the General Regulations under the Act. One of the primary findings was a breach of Section 22.1 of the General Regulation, which concerns material facts. Under this section, a broker or salesperson representing a client is required to take reasonable steps to determine the material facts relating to an acquisition or disposition of real estate. They must then disclose these facts to the client as soon as possible and advise the client to consider how those facts might affect their decision to proceed. The committee found that Kerkhoff failed to take these steps or, in the alternative, failed to refer the clients to a professional who could provide accurate advice on the tax.

Furthermore, the broker was found to be in violation of Section 5 of the Code of Ethics, which deals with misrepresentation. The regulation mandates that registrants must make their best efforts to ensure that any representations are accurate and not misleading. While the actual purchase price of the home was stated accurately, the failure to inform the clients of the additional $201,084.07 tax effectively misrepresented the total amount they would be required to pay to complete the transaction. The committee concluded that by failing to provide this information, the broker had not met the standard of making his best efforts to ensure his representations were not misleading.

The ethical obligations of a real estate professional were also central to the findings under Sections 8 and 9 of the Code of Ethics. Section 8 requires a registrant to promote and protect the best interests of their clients. The committee determined that failing to disclose a massive tax obligation and failing to conduct the necessary due diligence to identify that obligation was a direct failure to act in the best interests of the buyers. Additionally, Section 9 requires that a registrant provide conscientious and competent service, demonstrating reasonable knowledge, skill, and judgment. The broker’s incorrect belief that the tax had expired was viewed as a failure to demonstrate the required professional knowledge and competence expected of a registered broker in Ontario.

The decision also highlighted a breach of Section 11 of the Code of Ethics, which governs the requirement to refer clients to other services. This section dictates that if a registrant is not able to provide services with the necessary knowledge or skill, or if they are not authorized by law to provide specific advice, they must advise the person to obtain services from someone else. By not encouraging the buyers to seek legal or tax advice when he himself was misinformed about the status of the provincial tax, Kerkhoff failed to fulfill this duty. This specific failure was identified as a contributing factor to the buyers being blindsided by the tax bill just days before their closing date.

As a result of these findings, the Discipline Committee ordered a multi-part penalty. Marius Kerkhoff was ordered to pay a fine of $12,000 to the Real Estate Council of Ontario. This fine must be paid no later than 120 days after the date of the decision, which sets the deadline for May 15, 2026. In addition to the monetary penalty, the broker is required to undergo further professional education. He must successfully complete the course titled Introduction to TRESA, which covers the requirements and standards of the Trust in Real Estate Services Act. Proof of completion must be provided to the regulator within 180 days of the decision date.

The matter was resolved through an Agreed Statement of Facts and Penalty, meaning that the broker acknowledged the facts of the case and the resulting violations of the provincial regulations. This process included a waiver of a full hearing, as both the Real Estate Council of Ontario and the respondent agreed upon the terms of the settlement. The Chair of the Discipline Committee reviewed the agreed terms and determined that they were appropriate given the circumstances of the case. The decision was formally released and became effective in mid-January, marking the conclusion of this specific regulatory proceeding.

Read more cases about proceedings in regulated professions here.