The Ontario Superior Court of Justice has released a decision regarding the financial consequences for a buyer who fails to complete a commercial real estate transaction1. In the case of James D. Taylor Holdings Ltd. v. WJ Groundwater Canada Limited, Justice R.E. Charney granted a summary judgment in favor of the sellers, awarding them more than $808,000 in damages. The ruling is an example of established law regarding what happens when a property is resold for a significantly lower price than the original contract following a buyer’s breach of contract.

The dispute began in early 2022 when James D. Taylor Holdings Ltd. and James Darcy Taylor listed a vacant industrial property in the Township of Scugog, within the Town of Port Perry, Ontario. The property, which consisted of undeveloped land with no structures, was positioned in an industrial area and was originally listed for $2.5 million. On January 19, 2022, WJ Groundwater Canada Limited entered into an Agreement of Purchase and Sale to buy the land for $2.4 million. The buyer intended to use the site to park and store drilling rigs and to build a shop for equipment servicing.

The agreement included a standard due diligence period, granting the buyer fourteen days to inspect the property. This period was later extended by an additional seven days. Before the final deadline, the buyer delivered a written waiver, officially confirming that they were satisfied with the inspection and making the agreement firm and binding. As part of this process, the buyer paid a total deposit of $100,000 to be held by the real estate agent. At this stage, both parties were legally obligated to close the transaction on the scheduled date of April 15, 2022.

However, just four days before the closing date, the buyer notified the sellers through legal counsel that they would not be completing the purchase and would be backing out of the deal. The buyer claimed they had only recently finished a review of the local zoning and concluded that the property’s current zoning did not permit their intended industrial use. While the buyer considered the transaction to be at an end, the law viewed this as a repudiation of a firm contract. Because the buyer admitted they failed to close the deal, the subsequent legal proceedings focused entirely on the amount of money the sellers were owed in damages.

Immediately following the collapse of the deal, the sellers relisted the property in May 2022 with the same agent and at the same price. They soon received a conditional offer from a different buyer for approximately $1.928 million. The sellers countered this offer, and eventually, the parties agreed on a price of $2.11 million. This second deal was also conditional on a thirty day due diligence period. Ultimately, this second buyer decided not to proceed, and the agreement became void by June 2022.

As the months passed, interest in the property appeared to wane. By mid-July 2022, the sellers reduced the listing price to $2.45 million but received no further offers for several months. In September 2022, a commercial tenant of the sellers offered $1.5 million. The sellers attempted to negotiate, countering at $2.1 million (based on the previous conditional offer price), but the prospective buyer did not accept and made no further attempts to purchase the land. Despite another price reduction to $2.3 million in October 2022, the property sat on the market for the remainder of the year without a single inquiry.

Faced with a property that was not selling, the sellers took their real estate agent’s advice to lower the price significantly. On January 19, 2023, exactly one year after the original deal with WJ Groundwater, the sellers relisted the property for $1.4 million. The listing was explicitly described as being aggressively priced for a fast sale. This strategy worked quickly; within one day, they received an offer for $1.5 million. Although the sellers tried to negotiate the price up to $1.54 million, the buyer refused to budge. The sellers accepted the $1.5 million offer on January 24, 2023, and the sale officially closed two months later.

The core of the legal battle involved the $900,000 difference between the original $2.4 million contract and the final $1.5 million sale price. The buyer argued that the sellers had engaged in an improvident sale, meaning they sold the property for much less than it was actually worth. They contended that the $900,000 loss was the result of the sellers’ failure to properly mitigate their damages and argued that the market value of the land was still closer to $2.2 million at the time of the final sale.

To support this argument, the buyer submitted an expert appraisal report from a professional appraiser who valued the property at $2,240,000 as of early 2023. The buyer’s legal team argued that the court should use expert appraisals to determine the market value on the date the deal was supposed to close, rather than simply looking at the eventual resale price. They characterized the final $1.5 million sale as a fire sale driven by the sellers’ desperation rather than a true reflection of the market.

Justice Charney rejected the buyer’s approach, noting that it was based on a misreading of established legal principles in Ontario. The court explained that when a buyer defaults on a real estate transaction, the seller is generally entitled to the loss of bargain, which is the difference between the original contract price and the eventual resale price. If a property is sold on the open market in an arm’s length transaction to a third party, that sale price is considered the best evidence of market value.

The judge emphasized that the burden of proof lies with the buyer to show that a seller failed to take reasonable steps to mitigate their losses. In this case, the sellers had listed the property on the Multiple Listing Service (MLS) for nine months. They had gradually reduced the price and entertained multiple offers. Justice Charney pointed out that the property is only worth what someone is willing to pay for it. The fact that the property sat at a listing price of $2.3 million for three months without any interest strongly suggested that the buyer’s expert appraisal of $2.24 million did not reflect the reality of the market at that time.

Furthermore, the court noted that the buyer’s expert report only critiqued the valuation methodology of the sellers’ appraiser; it did not identify any specific flaws in the actual marketing or sales process. Under Ontario law, to prove a failure to mitigate, a defendant must provide evidence from a professional showing that specific shortcomings in the sale process actually caused the lower price. Because the buyer’s expert did not suggest that the sellers should have marketed the property differently or that a higher price could have been achieved through different steps, their argument failed.

While the court ruled in favor of the sellers on the primary damage claim, it did side with the buyer regarding certain carrying costs. The sellers had sought nearly $19,000 for lawn maintenance and snow removal. However, it was revealed during cross examination that the individual seller had billed his own corporation for these services. The judge ruled that a plaintiff cannot pay themselves for property maintenance and then claim that amount as damages against a defendant. The court also rejected a claim for the cost of an appraisal report, characterizing it as a litigation expense rather than a cost of carrying the property.

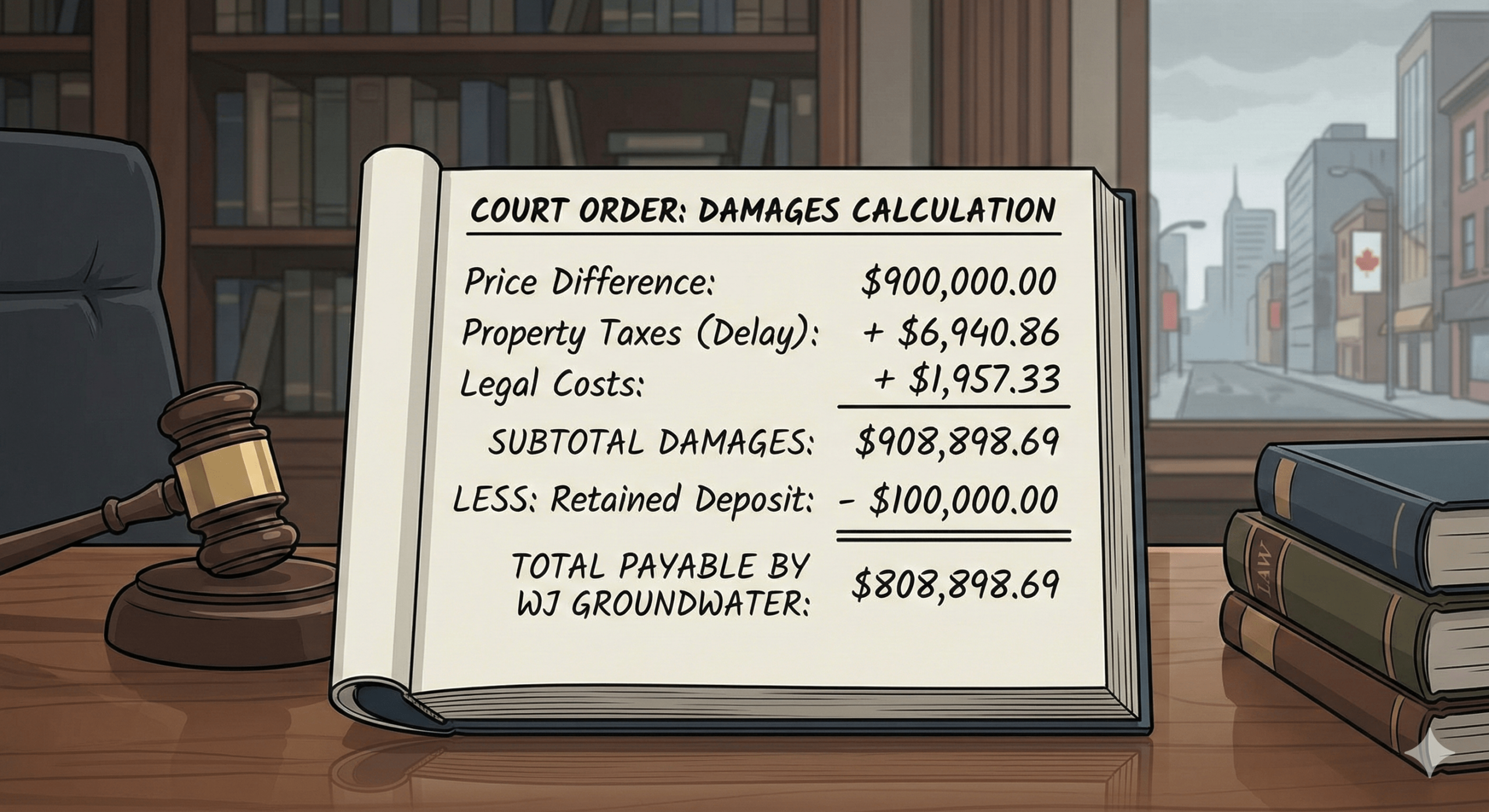

In the final calculation, the court started with the $900,000 price difference and added $6,940.86 for property taxes incurred during the delay and $1,957.33 in related legal costs. This brought the total damages to $908,898.69. After subtracting the $100,000 deposit that the sellers had already retained, the court ordered WJ Groundwater Canada Limited to pay the remaining balance of $808,898.69.

The decision serves as a reminder of the substantial financial risks associated with walking away from a firm Agreement of Purchase and Sale. In a fluctuating real estate market, a buyer who defaults may find themselves liable for the entire difference if the property value drops before a resale can be finalized. The court’s reliance on the actual resale price over theoretical expert appraisals highlights the heavy burden placed on defaulting buyers to prove that a seller’s mitigation efforts were unreasonable.

Read about more real estate cases here.