The Small Claims Court in Toronto recently addressed a complex dispute involving a mortgage discharge and the specific fees a lender is permitted to charge after a mortgage has matured1. This case arose when the Estate of Enrico Caruso Giovanni and Catherine Jeanne Rhodes sought the reimbursement of several thousand dollars in fees that were added to their mortgage discharge statement by Shedden Investments Inc., Jeunesse Development Corp., and Helen Strathman. The primary conflict centered on whether the borrowers had agreed to renew their mortgage or if the lenders were justified in charging extension fees and interest penalties when the homeowners sought to pay off the balance.

The financial relationship between the parties began on May 31, 2016, when Enrico Caruso Giovanni and Catherine Jeanne Rhodes entered into a one year mortgage for $300,000. The mortgage carried a significant interest rate of 12.75 percent per annum and was set to mature on June 1, 2017. As the maturity date approached and eventually passed, the mortgage remained unpaid. According to the evidence presented at trial, the borrowers had spent several weeks attempting to contact the lenders to discuss renewal options or a discharge. Catherine Jeanne Rhodes testified that she and her late husband had made numerous phone calls and left various messages over a month and a half period but received no response from the lenders until well after the mortgage had matured.

It was not until July 10, 2017, more than a month after the maturity date, that the lenders finally responded through their legal counsel. They sent an email offering mortgage renewal terms that included a renewal fee of $8,500 plus legal fees of $847.50. The lenders provided the homeowners with a very narrow window of only 48 hours to sign the agreement and return it with post-dated cheques. This sudden demand for a decision created a point of friction that eventually led to the litigation. Later that same evening, Enrico Caruso Giovanni replied to the lenders’ lawyers. In his email, he expressed frustration at how long it had taken to receive the documentation and noted that returning a signed agreement within two days would be a significant challenge. He specifically stated that they would need an extension to that deadline so that their own legal counsel could review the documents. He also informed the lenders that their home was on the market and being shown to potential buyers.

The lenders interpreted this reply as an indication that the homeowners intended to renew the mortgage. However, the homeowners maintained that they were simply asking for more time to consider their options and were shocked by the high fees associated with the renewal offer. Instead of signing the renewal, the homeowners continued to look for better mortgage options and eventually requested a discharge statement on July 21, 2017, so they could pay off the mortgage in full. When the lenders provided the final discharge statement in August 2017, it included the $8,500 renewal fee, the legal fees for the renewal, and a prepayment bonus equal to three months of interest. To clear the title of their home and finalize their financial affairs, the plaintiffs paid the full amount of $327,934.61 under protest and then filed a claim to recover what they believed were unauthorized charges.

Before the court could address the merits of the fees, it had to resolve two significant preliminary legal hurdles raised by the lenders. First, the lenders argued that the claim was barred by the two year limitation period. They contended that the time for filing a lawsuit began on June 1, 2017, when the mortgage matured. Since the claim was not issued until July 2019, the lenders argued it was too late. Deputy Judge L-K. Hum disagreed with this position, ruling that the limitation period only began to run when the discharge statement was delivered in August 2017. It was only at that point that the homeowners became aware of the specific additional charges they were being forced to pay. Therefore, the claim was found to be within the allowable timeframe.

The second procedural issue involved the naming of the plaintiffs. Catherine Jeanne Rhodes had been omitted from the initial claim form due to a clerical error and was only added later. The lenders argued that this addition happened after the limitation period had expired. The court found that this was an obvious mistake in completing the Small Claims Court forms and noted that the narrative of the original claim clearly referred to “Plaintiffs” in the plural. The judge ruled that the lenders knew or should have known there were two plaintiffs and allowed the correction of the record, noting that the lenders suffered no actual prejudice from the late formal addition of her name.

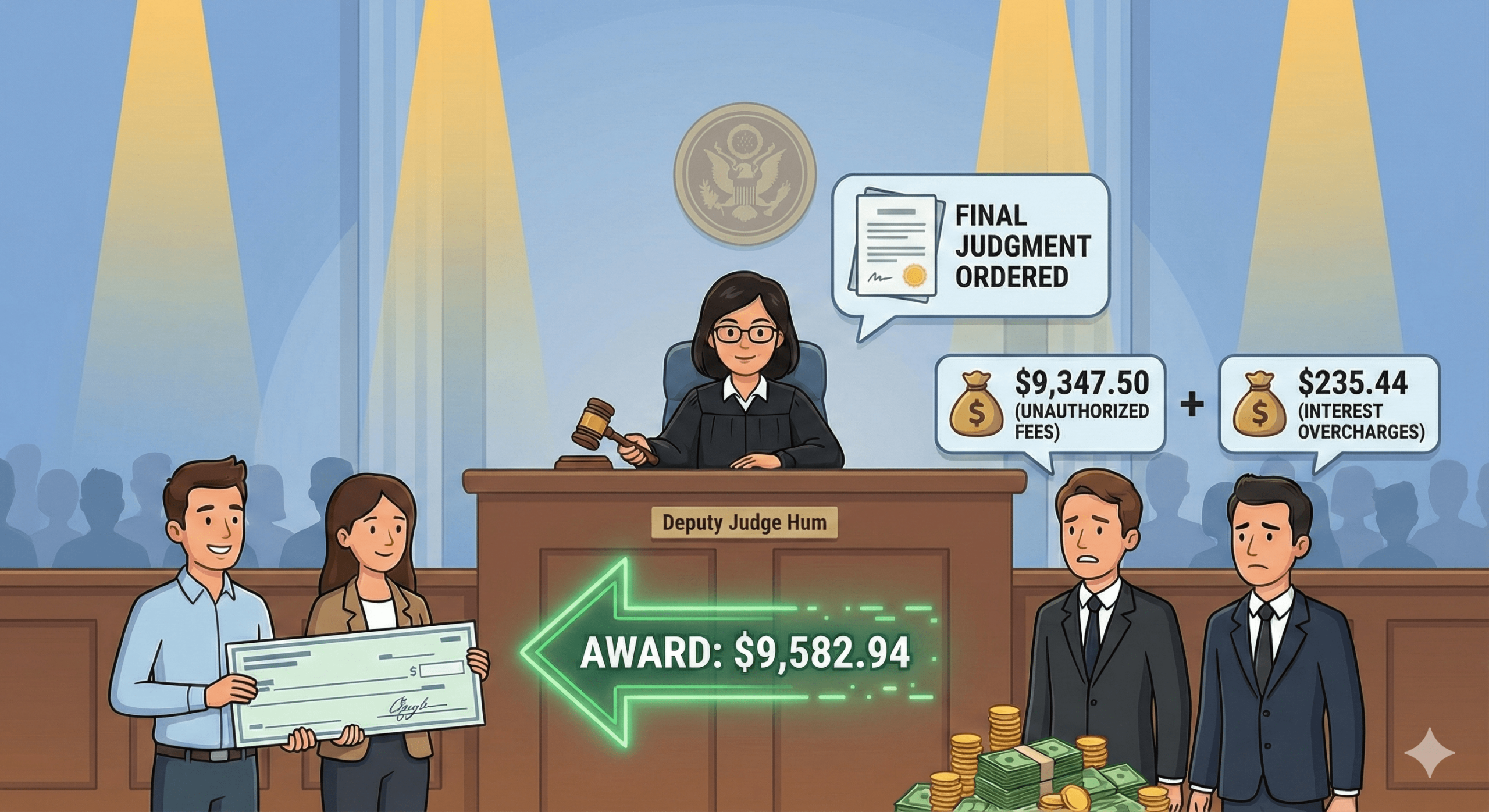

Once these preliminary matters were resolved, the court turned to the core of the dispute: the $9,347.50 in renewal and legal fees. The lenders argued that the email sent by Enrico Caruso Giovanni constituted a request for an extension and that they had granted it. Blair Rose, a principal at the law firm representing the lenders, testified that while they never received a signed agreement or post-dated cheques, it was their standard practice to assume a renewal was in place if a borrower asked for time and no enforcement action was taken. The court rejected this argument. The judge found that a plain reading of the email showed the homeowners were asking for an extension of the 48 hour deadline to review the offer, not an extension of the mortgage term itself. Because there was no signed agreement and no meeting of the minds regarding the renewal terms, the court ruled that the mortgage had not been renewed. Consequently, the lenders had no legal right to charge the $8,500 renewal fee or the associated legal fees.

The court then addressed the claim for the reimbursement of the three month interest penalty, which amounted to $9,941.52. The homeowners argued that this was an illegal penalty. However, the judge found in favor of the lenders on this specific point. Under the Mortgages Act and the terms of the original mortgage agreement, if a mortgage is not repaid by the maturity date, the lender is often entitled to three months of interest if the borrower eventually seeks to pay it off. The court noted that this penalty is generally permitted as long as the lender has not already taken steps to enforce the mortgage, such as issuing a notice of sale. Since the lenders in this case had remained passive and had not started enforcement proceedings, they were legally entitled to the three month interest bonus as a condition of the late discharge.

As a final calculation, the court looked at the interest that had accrued between the maturity date and the discharge date. The lenders had calculated this interest based on a principal balance that included the $8,500 renewal fee. Since the court determined that the renewal fee was invalid, the principal balance used for the interest calculation was too high. The judge ordered a refund of $235.44 to account for this overcharged interest.

In the final judgment, Deputy Judge Hum ordered the lenders to pay the plaintiffs a total of $9,582.94. This amount represented the $9,347.50 for the unauthorized renewal and legal fees plus the $235.44 in interest overcharges. The court also ordered the lenders to pay prejudgment and post-judgment interest on these sums dating back to 2017. Regarding the costs of the litigation, the judge awarded the homeowners $2,250.00. The judge remarked that the plaintiffs had been partially successful and that the legal counsel for both sides had provided helpful and professional assistance throughout the two day trial. This case serves as a detailed example of how courts interpret post-maturity communications and the strict requirements for lenders to prove that a mortgage has been formally renewed before they can levy significant administrative fees.

Read more Ontario legal news here.